The Humanoid Industrial Revolution: A Strategic Analysis of Transatlantic Robotics Convergence and Geopolitical Competition

Published:

Originally published on Substack.

The global industrial landscape is witnessing a structural shift as artificial intelligence transitions from purely cognitive, screen-based applications to embodied physical systems. This transformation, often termed “Physical AI,” represents the convergence of high-performance electromechanical hardware with foundational vision-language-action (VLA) models, creating a new class of general-purpose humanoid robots capable of operating within human-centric environments.1 As of early 2026, the sector has moved beyond the “peak hype” of laboratory demonstrations into a pivotal phase of commercial deployment and industrial scaling.3 The acceleration of this industry is driven by a unique synergy between the maturation of the electric vehicle (EV) supply chain, breakthroughs in end-to-end neural network training, and a critical global labor shortage in manufacturing and logistics sectors.3 For investors and policy makers, the humanoid robotics market is no longer a speculative future but a core component of national productivity and sovereign technological autonomy.

The Global Macro-Economic Framework for Humanoid Adoption

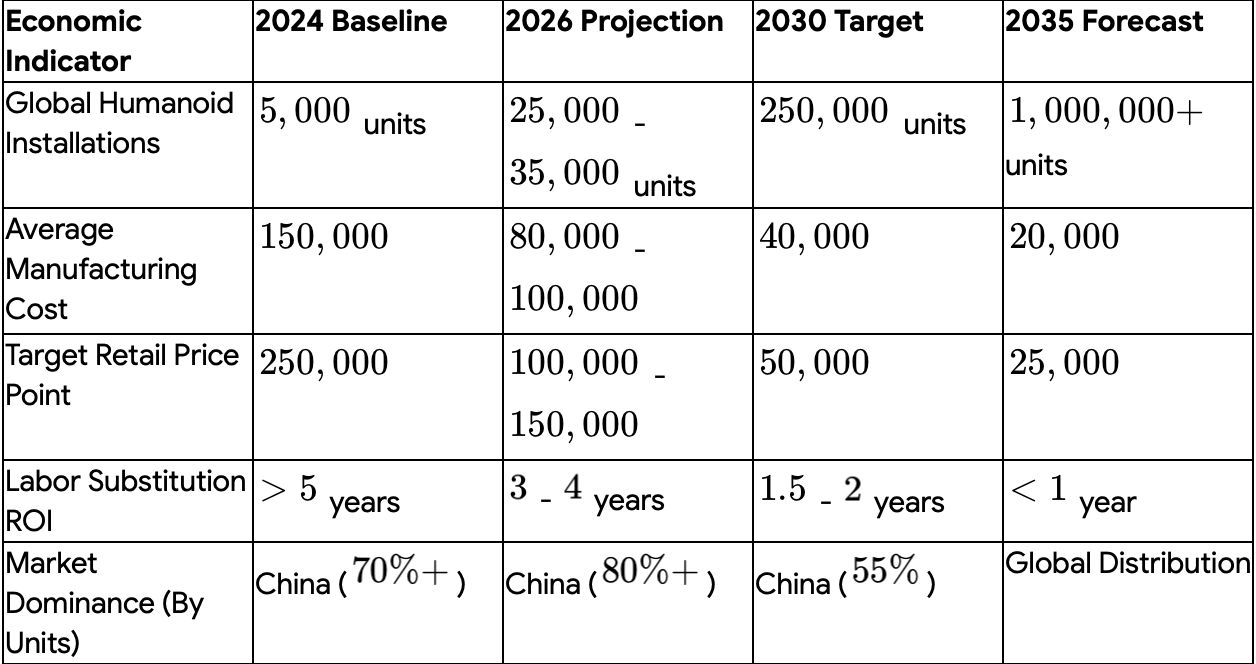

The humanoid robotics market is projected to expand from a valuation of approximately million in 2024 to over billion by 2033, representing a compound annual growth rate (CAGR) of .6 Other estimates from financial institutions such as Goldman Sachs and Morgan Stanley suggest even more aggressive trajectories, with the potential for the market to reach between billion and billion by 2035, and a long-term total addressable market (TAM) that could eventually be measured in trillions as robots integrate into every facet of the global economy.4 This growth is not merely a result of technological progress but is fundamentally anchored in demographic realities. Falling fertility rates and aging populations across the G7 and East Asia are creating structurally smaller workforces, leading to persistent upward pressure on labor costs and a corresponding shift in corporate strategy from operational expenditure (OpEx) on wages to capital expenditure (CapEx) on automated labor.5

The current distribution of the market reveals a stark geopolitical divide. As of late 2025, Chinese manufacturers have achieved a dominant position, accounting for over of all humanoid installations worldwide.4 This lead is not due to a superiority in cognitive AI—where the United States remains the leader—but rather a superior ability to iterate hardware and leverage a vertically integrated electronics and EV supply chain.9 However, startups in the United States and Europe are carving out high-value niches focused on complex reasoning, safe human-robot interaction (HRI), and integration into heavily regulated industrial and domestic sectors.4

The Chinese Benchmark: Acceleration through Supply Chain “Involution”

The Chinese humanoid ecosystem is characterized by what local observers call “involution”—an intense, hyper-competitive environment where thousands of startups and established tech giants compete for dominance, leading to rapid technological refinement and cost reduction.10 Companies like AgiBot (Zhiyuan Robotics) and Unitree Robotics have set the global pace for production, with AgiBot reaching a milestone of units produced by early 2026.11 The pace of this transition is unprecedented: it took AgiBot nearly two years to reach its first units, but the jump from to was completed in just three months.11

The Adjacency of the EV Supply Chain

The structural advantage of the Chinese robotics sector lies in its “structural identity” with the electric vehicle industry. Components such as high-torque servo motors, lithium-ion battery modules, power electronics, and environmental sensors (LiDAR and RGB-D cameras) are essentially the same for both cars and humanoids.7 China currently controls approximately of the key companies in the global supply chain for humanoid components and roughly of the world’s battery cell capacity.9 This density allows a Chinese startup to complete six hardware iterations in the time it takes a Western competitor to complete two.9

Strategic Industrial Clusters: T-Chain and H-Chain

The Chinese market is organized around two primary technological clusters: the “Tesla Chain” (T-Chain) and the “Huawei Chain” (H-Chain).12 The T-Chain focuses on high-performance actuators and thermal management, with suppliers like Sanhua Intelligent and Tuopu Group providing the mechanical foundations for platforms like Tesla’s Optimus.12 Conversely, the H-Chain emphasizes the “HarmonyOS” ecosystem and AI integration, utilizing iFLYTEK for voice interaction and Leisai Intelligent for servo systems.12 These clusters ensure that even small startups have access to world-class components at a fraction of the cost available to Western firms.9

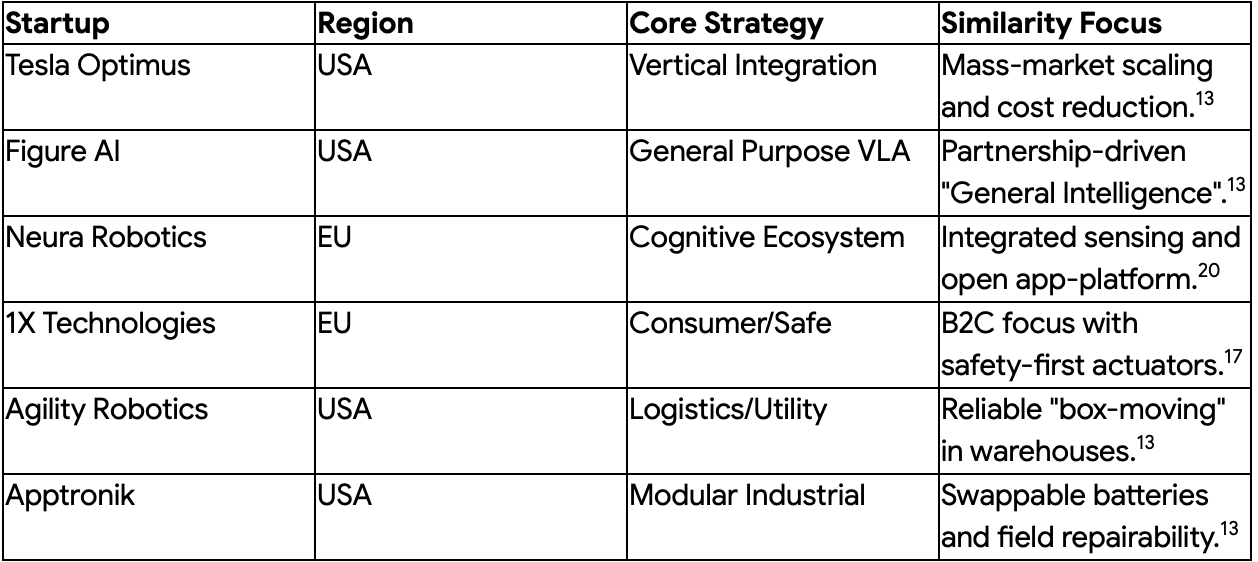

US Humanoid Startups: Compute Moats and Venture Scale

The United States approach to humanoid robotics is defined by “Venture Scale”—massive capital infusions aimed at building the most advanced cognitive “brains” for the robots.5 American startups are less concerned with producing the cheapest hardware and more focused on achieving “General Intelligence” in physical form.1

Tesla Optimus: The Vertical Integration Paradigm

Tesla is the most high-profile player in the US market, leveraging its expertise in AI inference, manufacturing automation, and energy storage.13 Elon Musk has positioned Optimus as potentially more valuable than Tesla’s automotive business, aiming for a retail price of under and mass production of million units annually.13 Optimus Gen 2 and Gen 3 have demonstrated significant breakthroughs in end-to-end learning, performing tasks such as cooking, cleaning, and industrial assembly by watching human demonstrations rather than through explicit coding.16 The strategy is to turn the “car” (a robot with four wheels) into a “humanoid” (a robot with two legs), using the same Full Self-Driving (FSD) neural networks and the Dojo supercomputer for training.13

Figure AI: The Collaborative Hyperscale Model

Figure AI represents the fastest-growing humanoid valuation in history, reaching billion by late 2025.13 Figure’s success is built on a “consortium” model, with backing from Microsoft, NVIDIA, OpenAI, Jeff Bezos, and Intel.4 Their Figure 02 and Figure 03 models utilize a proprietary “Helix” VLA model, which employs a dual-system architecture: System 1 operates at Hz for low-level motor control and reflexes, while System 2 operates at – Hz for high-level reasoning and task planning.13 This allows the robot to handle delicate tasks, such as manipulating objects with tactile sensors capable of detecting forces as small as grams.13

Pragmatic Industrialists: Agility Robotics and Apptronik

While Tesla and Figure chase general-purpose utility, Agility Robotics and Apptronik have focused on immediate commercial viability in the logistics sector.14 Agility’s Digit robot is currently the leader in real-world warehouse deployment, with active pilots at Amazon and GXO Logistics.4 Digit is designed to fit into existing workflows, performing “tote-to-person” tasks and handling material in environments where traditional automation is too rigid.4 Apptronik’s Apollo robot emphasizes “field serviceability” and modularity, using swappable -hour batteries to ensure near-continuous operation on factory floors.13

European Humanoid Ecosystem: Precision Engineering and Regulatory Moats

European humanoid startups are building a competitive advantage through high-precision engineering and a focus on “Cognitive Robotics”—machines that can safely interact with humans in unstructured domestic and healthcare settings.6 The European strategy is heavily influenced by the EU AI Act, which mandates transparency and safety, potentially creating the world’s most trusted platforms for human-centric applications.21

Neura Robotics: The Cognitive Pioneer

Metzingen-based Neura Robotics has emerged as Europe’s leader by adopting a “one-device” philosophy, viewing their 4NE1 humanoid as a “smartphone with arms and legs”.20 Neura’s core innovation is the “Neuraverse” ecosystem, a platform that allows developers to create apps for robots using an open development environment and a security/operating system.20 Their MAiRA and 4NE1 platforms are equipped with human-like sensing—vision, spatial audio processing, and -DOF force-torque sensors—allowing them to work alongside humans without protective cages.20

1X Technologies: The Home Assistant Vision

Norway’s 1X Technologies (formerly Halodi Robotics) is betting on the consumer home market.17 Backed by the OpenAI Startup Fund, 1X is developing the NEO robot, which is designed with “muscle-like” actuators for safe interaction in domestic environments.1 1X is the first company to accept consumer pre-orders for a humanoid at a price point, targeting 2026 for initial deliveries.17 Their focus on “cloning human thought and behavior” intofoundation models for safety distinguishes them from purely industrial players.17

PAL Robotics and Shadow Robot: Niche Excellence

Spain’s PAL Robotics and the UK’s Shadow Robot Company represent the “deep tech” end of the European market. PAL’s KANGAROO platform is designed for dynamic locomotion and embodied AI research, while Shadow Robot’s “Shadow Hand” remains the industry standard for dexterous manipulation, utilizing optical D sensors and magnetic Hall effect arrays to provide human-level tactile feedback.23

Similarity Mapping: Cross-Regional Convergence in Humanoid Strategy

Despite differences in funding and geographic origin, a “Transatlantic Consensus” is emerging on the technical and commercial requirements for humanoid success. US and European startups are converging on several key architectural and business strategies.

Technical Convergence: The Physical AI Stack

All leading startups have transitioned from traditional, pre-programmed control systems to end-to-end neural networks.1 The standard “Physical AI” stack now consists of:

Foundational Models: Large Vision-Language-Action (VLA) models that allow robots to understand natural language commands and map them to physical motor outputs.2

Sim-to-Real Transfer: Utilizing high-fidelity digital twins and simulation environments (like NVIDIA Isaac Lab) to train robots on millions of variations of a task before they ever touch a real-world object.13

Multimodal Sensing: The integration of LiDAR, stereo cameras, and tactile skins to provide “contextual understanding” of the environment.4

Business Model Convergence: Robotics-as-a-Service (RaaS)

To overcome high upfront capital costs, startups on both sides of the Atlantic are adopting RaaS models.13 By charging an hourly rate—typically around to per hour—or a monthly subscription (e.g., for home units), these companies align their incentives with the user’s need for uptime and reliability.2 This model effectively turns the robot into a “liquid labor” asset that can be scaled up or down based on seasonal demand.25

Supply Chain Deep Dive: The Actuator and Component Moat

For investors, the most “investable” part of the humanoid revolution in 2026 is often the component layer rather than the robot OEMs themselves.5 The “Three Bs” of the humanoid supply chain—Brains (compute), Bodies (actuators), and Batteries—represent the critical bottlenecks for the industry.5

Brains: The Compute Infrastructure

Humanoids require massive on-board compute for real-time inference. NVIDIA’s Jetson Thor platform, released in 2025, has become the de facto standard, providing the performance of prior generations.2 The software “brain” is increasingly moving toward decentralized identities (DIDs) and programmable wallets for robots, allowing them to autonomously pay for charging or software updates via blockchain protocols.27

Bodies: The Actuator Market

The actuator is the single most expensive component of the humanoid, often accounting for to of the bill of materials (BOM).3 While Chinese suppliers like AgiBot have developed their “PowerFlow” integrated joints for peak torque density, Western suppliers like Maxon (Switzerland), Harmonic Drive (Japan/USA), and Kollmorgen (USA) maintain a lead in precision and reliability.28

Maxon Motor (CH): Specialized in high-efficiency joints (HEJ) that integrate motors, gearheads, sensors, and electronics into a single IP67-rated housing, capable of Nm peak torque.29

Kollmorgen (USA): Their TBM2G series provides frameless motors designed specifically for harmonic gearing, optimizing for torque density and weight in human-scale joints.30

Harmonic Drive (Global): Remains the monopoly holder for high-precision strain wave gearheads, though Chinese competitors like Green Harmonics are rapidly gaining domestic market share ( in China).12

Batteries: The Energy Density Challenge

Humanoids are significantly less energy-efficient than humans, requiring high-density lithium-ion packs to survive an -hour shift.5 While battery costs have fallen in ten years, the challenge remains thermal management during high-torque events.5 Tesla and Chinese firms like BYD have a strategic advantage here, as they can leverage their existing automotive battery production lines to reduce costs by compared to standalone robotics startups.9

Geopolitical Implications: The American Security Robotics Act and Beyond

Policy makers are increasingly viewing humanoid robotics through the lens of national security and economic sovereignty.10 The “robotics race” with China is now being equated to the semiconductor race in terms of strategic importance.25

US Legislative Response

In March 2026, the US Congress introduced the American Security Robotics Act.33 Proposed by Senators Tom Cotton and Chuck Schumer, the bill would:

Ban Federal Procurement: Prohibit the US government from purchasing or operating humanoid robots made by Chinese firms.33

Mitigate Data Risks: Cite concerns that Chinese humanoids could serve as surveillance tools or be remotely controlled by foreign adversaries.33

Protect Domestic Industry: Guard American research from “market flooding” by subsidized Chinese competitors.33

Additionally, the United States has expanded Section 301 tariffs to include Chinese-made robotics and semiconductors, with initial rates set to increase significantly by mid-2027 to discourage reliance on the Chinese “T-Chain”.34

The EU Regulatory Stance

Europe is pursuing a “Third Way,” focusing on the EU AI Act and the Digital Omnibus on AI Regulation.21 While the US focuses on defense and competition, the EU is prioritizing ethical frameworks:

Prohibited Practices: The AI Act bans “harmful manipulation” and “emotion recognition” in workplaces, which could limit the deployment of certain Chinese or US bots that use facial analysis for productivity tracking.21

Safety Certification: The revised ISO 10218-1/2:2025 and ANSI/A3 R15.06-2025 standards have shifted from certifying the “robot” to certifying the “deployment,” placing more responsibility on the factory owner to ensure a safe collaborative environment.36

Horizon Europe and Sovereign Funding

To counter the massive subsidies of the Chinese government ( billion over 20 years), the European Commission has allocated over million in late 2025 for “Cognitive Computing” and “Soft Robotics” research.37 The goal is to build “tech sovereignty” in AI, data, and robotics, ensuring that European industry remains competitive in Wave 2 (consumer/developer) and Wave 3 (medical/elder care) applications.3

The Future of Work: The National Autonomous Work Index (NAWI)

A novel economic framework is emerging for policy makers to measure national strength: the National Autonomous Work Index (NAWI), also known as the “Autonomous Workforce of the Nation” (AWN).25 This metric measures the total annual hours of productive work performed by robots and automated systems.25

The National Time Dividend

Policy makers are exploring the concept of a “National Time Dividend”—where the deflationary pressure created by humanoid productivity (e.g., reduction in the cost of domestic appliances) is distributed to the public through lower costs of living rather than direct taxation.25 This approach aims to stabilize the economy as repetitive manual jobs shrink by to globally.1

DARPA and Defense Innovation

The US Department of Defense, through the DARPA Triage Challenge, is driving humanoid innovation into high-risk medical and disaster-response scenarios.40 By November 2026, the final event of this challenge will test whether autonomous systems can perform medical triage in mass-casualty incidents, providing a “dual-use” pathway for humanoid technology to move from the battlefield to civilian emergency services.40

Conclusion: Actionable Insights for Investors and Policy Makers

The humanoid robotics sector has reached a genuine growth inflection point. The convergence of Physical AI software with mature hardware supply chains has made mass adoption a 2027–2030 reality.2

For Investors:

Pivot to the Component Layer: The most defensive “moats” are held by precision actuator manufacturers and specialized AI chip designers (the “Three Bs”).5

Prioritize Data-Rich OEMs: Firms like Figure AI, Tesla, and Neura Robotics that are actively amassing “real-world spatial data” through enterprise pilots will hold the long-term software advantage.10

Sectoral Timing: Invest in “Wave 1” automotive and logistics specialists now, but keep a close watch on “Wave 2” consumer and “Wave 3” healthcare platforms for the 2028 horizon.3

For Policy Makers:

Subsidize the Supply Chain, not just R&D: To counter China’s lead, the US and EU must incentivize domestic “Actuator Hubs” and battery capacity specifically for mobile robotics.9

Streamline Regulatory Compliance: The EU must ensure the AI Act does not become a barrier to adoption, while the US must coordinate state-level AI laws to provide a “minimally burdensome” national framework for startups.22

Measure “Sovereign Work-Hours”: Adopt metrics like the NAWI to track national productivity and ensure that the “Robotics Boom” translates into a structural reduction in the cost of living for citizens.25

The humanoid revolution is the final stage of the digital transformation. By embedding intelligence into physical form, we are unlocking the largest total addressable market in history.8 Success will depend on the ability to balance rapid iteration with uncompromising safety and national security.

Reference:

The Dawn of Humanoid Robots and Physical AI - Leo Wealth, accessed March 31, 2026, https://leowealth.com/insights/the-dawn-of-humanoid-robots-and-physical-ai/

Robotics: AI Moves into the Physical Economy - Global X ETFs, accessed March 31, 2026, https://www.globalxetfs.com/articles/robotics-ai-moves-into-the-physical-economy

The Global Humanoid Robots Market 2026-2036 - Advanced and Emerging Technology Market Research, accessed March 31, 2026, https://www.futuremarketsinc.com/the-global-humanoid-robots-market-2026-2036-3/

Humanoid Robot Market Size: $38B by 2035 — Growth Data & Forecasts - Blog, accessed March 31, 2026, https://blog.robozaps.com/b/market-size-for-humanoid-robots

AI gets physical: Innovation meets opportunity - Barclays Investment Bank, accessed March 31, 2026, https://www.ib.barclays/our-insights/series/impact-series/ai-gets-physical-innovation-meets-opportunity.html

Humanoid Robot Market Trends | Market Intelligence 2033, accessed March 31, 2026, https://www.skyquestt.com/report/humanoid-robot-market

A new era: physical AI and humanoids enter the stage - Betashares, accessed March 31, 2026, https://www.betashares.com.au/insights/a-new-era-robots/

Musk has a plan to make human labor obsolete. Billionaires are joining in., accessed March 31, 2026, https://www.washingtonpost.com/technology/2026/03/27/musk-optimus-robot-physical-ai/

China’s humanoid robot cluster – 80 percent global market share ..., accessed March 31, 2026, https://xpert.digital/en/chinas-humanoid-robot-cluster/

Is China Leading the Robotics Revolution? | ChinaPower Project, accessed March 31, 2026, https://chinapower.csis.org/china-industrial-robots/

AGIBOT Reaches 10,000 Units as Real-World Demand for Robots Accelerates, accessed March 31, 2026, https://www.prnewswire.com/news-releases/agibot-reaches-10-000-units-as-real-world-demand-for-robots-accelerates-302728295.html

Three core supply chains of humanoid robots (Tesla Chain, Huawei Chain, Unitree Chain), accessed March 31, 2026, https://www.yicaiglobal.com/star50news/2025_03_056800594033476370453

30+ Humanoid Robot Companies Ranked [2026] - Blog - Robozaps, accessed March 31, 2026, https://blog.robozaps.com/b/humanoid-robot-companies

Top 12 humanoid robotics companies to watch in 2026 - Standard Bots, accessed March 31, 2026, https://standardbots.com/blog/humanoid-robotics-companies

Robozaps Blog - Humanoid Robotics News & Insights, accessed March 31, 2026, https://blog.robozaps.com/

Humanoids on the move: How 2025 became the breakthrough year ..., accessed March 31, 2026, https://techequity-ai.org/humanoids-on-the-move-how-2025-became-the-breakthrough-year-for-ai-driven-robotics/

12 Fastest Growing Robotics Companies and Startups - Landbase, accessed March 31, 2026, https://www.landbase.com/blog/fastest-growing-robotics-companies

Figure vs Apptronik vs Agility Robotics - Sacra, accessed March 31, 2026, https://sacra.com/research/figure-vs-apptronik-vs-agility-robotics/

31 Best Humanoid Robots [2026 Ranked] - Blog, accessed March 31, 2026, https://blog.robozaps.com/b/best-humanoid-robots

NEURA Robotics x Made for Germany, accessed March 31, 2026, https://neura-robotics.com/neura-robotics-made-for-germany-initiative/

EU AI Act - Updates, Compliance, Training, accessed March 31, 2026,

https://www.artificial-intelligence-act.com/

The EU AI Act: A Story without a Plot? A Lack of Vision in the Digital AI Omnibus Proposal threatens constitutional AI Governance - Jean Monnet Saar, accessed March 31, 2026, https://jean-monnet-saar.eu/?p=322956

PAL Robotics | Home, accessed March 31, 2026, https://pal-robotics.com/

Humanoid Robotics Component Datasheet — Live Supplier, Pricing & Certification Updates, accessed March 31, 2026, https://humanoid.press/humanoid-press/datasheet/

The Autonomous Workforce of the Nation: A National Time-Bank Strategy - Liquid Labor, accessed March 31, 2026, https://www.liquid-labor.com/

Is robotics the next frontier for AI? | J.P. Morgan Asset Management, accessed March 31, 2026, https://am.jpmorgan.com/sg/en/asset-management/per/insights/market-insights/market-updates/on-the-minds-of-investors/is-robotics-the-next-frontier-for-ai/

physicalai Community Insights & Market Sentiment | Binance Square, accessed March 31, 2026, https://www.binance.com/en/square/hashtag/PhysicalAI

Robotic Actuator and Servo Motor Selection Guide - CubeMars, accessed March 31, 2026, https://www.cubemars.com/robotic-actuator-and-servo-motor-selection-guide.html

Powerful robot drives: Perfect solutions for modern robotics - Maxon Motor, accessed March 31, 2026, https://www.maxongroup.com/en-us/market-solutions/mobility-solutions/robotics

Humanoid Robots - Kollmorgen, accessed March 31, 2026, https://www.kollmorgen.com/en-us/solutions/robotics/humanoid-robots

maxon at the SPS 2025: New drive solutions for robotics, automation and mobility, accessed March 31, 2026, https://www.maxongroup.com/en-us/news-and-events/news/maxon-at-the-sps-2025-new-drive-solutions-for-robotics-automation-and-mobility-288150

Humanoid Robots 2025-2035: Technologies, Markets and Opportunities - IDTechEx, accessed March 31, 2026, https://www.idtechex.com/en/research-report/humanoid-robots/1093

US lawmakers to introduce bill to ban government use of Chinese ..., accessed March 31, 2026, https://virginiabusiness.com/us-lawmakers-to-introduce-bill-to-ban-government-use-of-chinese-robots/

USTR Issues Affirmative Determination in China Semiconductor Section 301 Investigation, accessed March 31, 2026, https://www.thompsonhinesmartrade.com/2026/01/ustr-issues-affirmative-determination-in-china-semiconductor-section-301-investigation/

The U.S. Imposes New Section 301 Tariffs on Chinese Semiconductors, accessed March 31, 2026, https://www.internationaltradeinsights.com/2025/12/the-u-s-imposes-new-section-301-tariffs-on-chinese-semiconductors/

Top Quadruped Robot Safety Standards and Risk Assessment for Industry 2026, accessed March 31, 2026, https://www.oxmaint.com/blog/post/quadruped-robot-safety-standards-2026

China to Invest 1 Trillion Yuan in Robotics and High-Tech Industries, accessed March 31, 2026, https://ifr.org/news/china-to-invest-1-trillion-yuan-in-robotics-and-high-tech-industries/

Horizon Europe: Digital — 2025 call results: 20 proposals funded, accessed March 31, 2026, https://hadea.ec.europa.eu/news/horizon-europe-digital-2025-call-results-20-proposals-funded-2026-02-20_en

Horizon Europe - funding digital technology and research, accessed March 31, 2026, https://digital-strategy.ec.europa.eu/en/activities/horizon-europe-funding-digital

Inside DARPA’s High-Stakes Challenge to Build Life-Saving Robots - eWeek, accessed March 31, 2026, https://www.eweek.com/news/darpa-challenge-life-saving-robots/

DARPA Triage Challenge, accessed March 31, 2026, https://www.darpa.mil/research/challenges/darpa-triage-challenge

Challenge Events - DARPA, accessed March 31, 2026, https://www.darpa.mil/research/challenges/darpa-triage-challenge/events

Sunny Cheung Testimony - U.S.-China Economic and Security Review Commission, accessed March 31, 2026, https://www.uscc.gov/sites/default/files/2025-02/Sunny_Cheung_Testimony.pdf

2026 AI Laws Update: Key Regulations and Practical Guidance - Gunderson Dettmer, accessed March 31, 2026, https://www.gunder.com/en/news-insights/insights/2026-ai-laws-update-key-regulations-and-practical-guidance