Unitree’s Trajectory Towards Hardware Dominance in Robotics

Published:

Originally published on Substack.

Content

Executive Summary

1. Introduction: Unitree's Strategic Trajectory in Robotics

2. Market Dynamics: Driving Hardware Commoditization and Accessibility

3. Investor Alignment: Capitalizing on Hardware and Ecosystem Integration

4. Team Capabilities: Engineering Prowess and Hardware Innovation

5. Policy Environment: Government Support for Hardware Manufacturing and Self-Reliance

Conclusion

Executive Summary

Unitree Robotics, a prominent Chinese innovator in legged robotics, is strategically positioning itself to become a dominant hardware company. This trajectory is not merely incidental but a deliberate outcome shaped by its aggressive market strategies, the foundational expertise of its team, the strategic alignment of its investors, and a supportive national policy framework. Unitree's core business model is evolving towards high-volume, cost-effective manufacturing and sales of robotic hardware. This approach aims to establish a broad installed base upon which future artificial intelligence (AI) and service layers can be built, thereby achieving commoditization and widespread adoption in the burgeoning global robotics market.

Key findings indicate that Unitree's aggressive pricing strategy, exemplified by the R1 at approximately $5,900, aims to commoditize robotics hardware, mirroring DJI's successful market penetration tactics in the drone sector. This strategy targets a broad market of developers, enthusiasts, and industrial users who prioritize accessible, high-performance physical platforms. Major Chinese tech and industrial giants, including Tencent, Alibaba, China Mobile, and Geely Capital, are backing Unitree. Their investments extend beyond mere capital, providing access to critical manufacturing ecosystems, AI infrastructure, and broader strategic integration, reflecting a shared belief in the foundational value of scalable robotics hardware.

Unitree's leadership, particularly CEO Wang Xingxing, possesses deep-rooted expertise in developing core robot components (motors, reducers, controllers, sensors) in-house. This engineering prowess enables the production of robust, low-cost hardware, which Wang explicitly identifies as a prerequisite for mass deployment, even as AI capabilities continue to mature. Finally, the Chinese government's "Made in China 2025" and 14th Five-Year Plan actively promote domestic robotics manufacturing, self-reliance in core components, and the rapid deployment of intelligent robots in industries. This provides Unitree with unparalleled state support, funding, and a conducive regulatory environment to scale its hardware production.

1. Introduction: Unitree's Strategic Trajectory in Robotics

Unitree Robotics has rapidly emerged as a significant player in the global robotics market, particularly known for its high-performance quadruped and humanoid robots. The company has garnered international attention through viral demonstrations and its notably aggressive pricing strategies, signaling a disruptive force in the industry. Its product portfolio ranges from advanced quadruped inspection solutions to ultra-lightweight humanoid robots, demonstrating a versatile approach to addressing various market needs.

In the context of robotics, a "hardware company" primarily focuses on the design, development, manufacturing, and sales of the physical robotic platforms and their core mechanical and electronic components. While software and artificial intelligence (AI) are integral to a robot's functionality, a hardware-centric model emphasizes the robot itself as the primary product and revenue generator. This approach aims for economies of scale in production and widespread physical deployment. This stands in contrast to a pure software or service model, where the physical robot might primarily serve as a vehicle to deliver a software-driven service, rather than being the core product. This report will systematically analyze how Unitree's market approach, investor alignment, internal team capabilities, and the prevailing policy environment in China converge to solidify its identity and future as a hardware-first robotics company.

2. Market Dynamics: Driving Hardware Commoditization and Accessibility

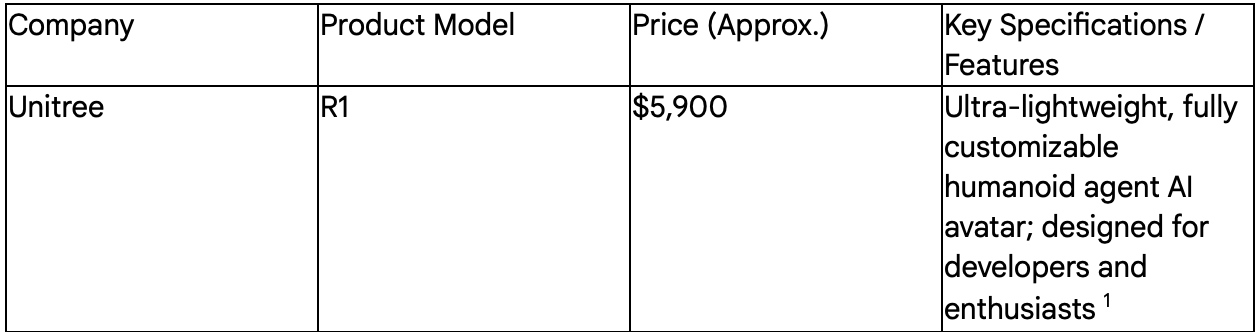

Unitree's market strategy is characterized by an aggressive pricing model designed to disrupt the existing robotics landscape. The company's R1 humanoid robot, for instance, is priced at approximately $5,900. This strategic pricing is not merely a discounting tactic but a deliberate push to lower the entry barrier for buyers, stimulate demand, and accelerate the creation of a broader commercial ecosystem. This approach draws direct comparisons to DJI's early market tactics in the drone industry, where significantly undercutting competitors was instrumental in establishing a dominant market position and capturing substantial market share. For example, Unitree's G1 robot is priced at $16,000, which substantially undercuts Tesla's Optimus, projected to range from $20,000 to $25,000, while offering competitive technical specifications such as running at 12 km/h and carrying over 40 kg.

The low pricing strategy is specifically designed to invite developers and enthusiasts to engage in tackling complex challenges, such as whole-body control and human-guided imitation, thereby fostering a vibrant community around Unitree's products. This indicates a strategic move to build an ecosystem around accessible hardware, reminiscent of how personal computers or smartphones created platforms for widespread software development. Unitree's products, including the G1, are explicitly designed as "research, development, and demonstration platform[s]". The G1 EDU model further supports "Secondary Development" and integrates an NVIDIA Jetson Orin module for enhanced computing power, positioning the physical robot as a versatile tool for innovation that appeals directly to academic and research institutions.The broader market demand within China is experiencing a significant surge, with Unitree and other domestic firms aiming for high-volume production (exceeding 1,000 units annually) to fulfill corporate requirements, particularly from state-owned enterprises. This clearly indicates a pathway towards large-scale industrial hardware deployment.

The global robotics market is projected for substantial growth, expanding from $53.2 billion in 2024 to an estimated $178.7 billion by 2033. The Chinese robotics market already holds the largest share globally, accounting for 51% of industrial robot installations in 2023, and is forecast to grow at a 23% annual rate through 2028, reaching $108 billion.Crucially, within the global robotics industry, the "hardware segment captures the majority share of the market". This dominance is attributed to the high demand for fundamental components such as sensors, actuators, and robotic arms, driven by their critical role in performance, precision, and efficiency in industrial robotics applications.

Unitree directly competes with established advanced players like Boston Dynamics and emerging giants like Tesla. While Boston Dynamics emphasizes "highly mobile robots" and commercializes platforms such as Spot and Stretch , and Tesla aims for mass production of its Optimus humanoid , Unitree's distinct competitive edge lies in its aggressive pricing combined with highly competitive technical specifications. The company's trajectory is described as "reminiscent of China's rapid rise in electric vehicles" , suggesting a strategic playbook of achieving market dominance through a combination of cost-effectiveness and rapid scaling of hardware production—a hallmark of China's manufacturing prowess.

The company's strategy of launching low-cost robots, explicitly marketing them as "entry level hardware" and "great developer platform[s]" , is a deliberate move to foster an external development ecosystem. This approach parallels DJI's successful tactic of undercutting competitors to establish market dominance, where the cultivation of a vast ecosystem of developers and hobbyists created applications and accessories dependent on DJI's core hardware. By making the physical robot highly accessible and developer-friendly, Unitree is strategically cultivating a community that will invest significant time and resources into developing applications and solutions specifically for Unitree's physical platforms. This creates a powerful network effect and substantial switching costs for users, effectively locking them into the Unitree hardware ecosystem. The lower price point dramatically reduces the barrier to entry for experimentation and innovation, which, in turn, accelerates the overall development and adoption of embodied AI by providing the necessary physical substrate. This suggests that Unitree views its hardware as the foundational layer for all future value creation. The "commoditization of AI robots" implies that the physical robot itself will transition into a widely accessible, potentially lower-margin product, with higher-margin opportunities expected to emerge from services, specialized applications, or the valuable data generated by a massive installed base of Unitree hardware. This positions Unitree as a potential "Android" of robotics hardware, enabling a diverse and dynamic software ecosystem to flourish on its affordable physical devices.

The global robotics market's "hardware segment captures the majority share". Unitree's CEO explicitly states, "Hardware still needs to be cheaper, be larger-scale and more reliable" for mass deployment, even while acknowledging that embodied AI is currently the "biggest obstacle". He further notes, "Current robot hardware is sufficient but embodied AI remains inadequate". This perspective challenges the common narrative that software is inherently superior and hardware is merely a commodity. However, in the domain of physical robotics, the robustness, cost-effectiveness, and reliability of the hardware directly determine the feasibility of widespread adoption and the ability to collect the real-world data essential for training advanced AI models. Unitree's intense focus on making hardware "cheaper, larger-scale and more reliable" is a direct and strategic response to the market's primary demand and a fundamental prerequisite for the "commoditization of AI robots". Without affordable and reliable physical platforms, even groundbreaking AI models cannot be widely deployed or generate the necessary data for continuous improvement. The "cost of hardware" is identified as a top concern for industrial users. By proactively addressing this critical barrier, Unitree is clearing the path for mass adoption. This "hardware-first" approach represents a calculated strategic bet that controlling the means of production for affordable, high-quality robots will yield long-term market leadership. It implies that while AI is the ultimate long-term goal, the immediate competitive advantage and the most viable path to scale lie in manufacturing excellence and cost leadership in physical robotics. This is a classic "picks and shovels" play, where Unitree positions itself to provide the essential tools (the robots themselves) for the impending AI revolution, rather than solely focusing on the "gold" (the AI models) itself.

Table 1: Unitree Product Portfolio & Pricing Comparison vs. Key Competitors

This table clearly illustrates Unitree's aggressive pricing strategy, particularly with the R1, which is significantly more affordable than anticipated competitor offerings like Tesla's Optimus. This direct, side-by-side comparison serves as strong empirical evidence for the report's central argument regarding Unitree's hardware-centric and commoditization strategy. The substantial price differential is visually compelling and directly reinforces the "DJI-like" market approach. This format helps the reader quickly grasp Unitree's strategic market positioning—namely, its focus on offering high-performance robots at substantially lower price points. This is a key driver for its potential hardware dominance. It also effectively showcases the breadth of Unitree's hardware portfolio, spanning both quadrupeds and humanoids. By clearly illustrating the current product landscape, the table sets the stage for a deeper discussion on the implications of Unitree's strategy for market share acquisition and the potential for a "race to the bottom" in robotics hardware pricing, which would ultimately accelerate the commoditization of the entire robotics sector.

3. Investor Alignment: Capitalizing on Hardware and Ecosystem Integration

Unitree has successfully completed multiple significant funding rounds, including a Series C round in May 2025 that valued the company at $2.95 billion. Another Series C round, led by major tech giants, approached 700 million RMB in financing, resulting in a post-investment valuation exceeding 12 billion RMB. The company has undergone a remarkable 11 rounds of financing since its establishment in 2016, signaling sustained and robust investor confidence in its long-term trajectory.

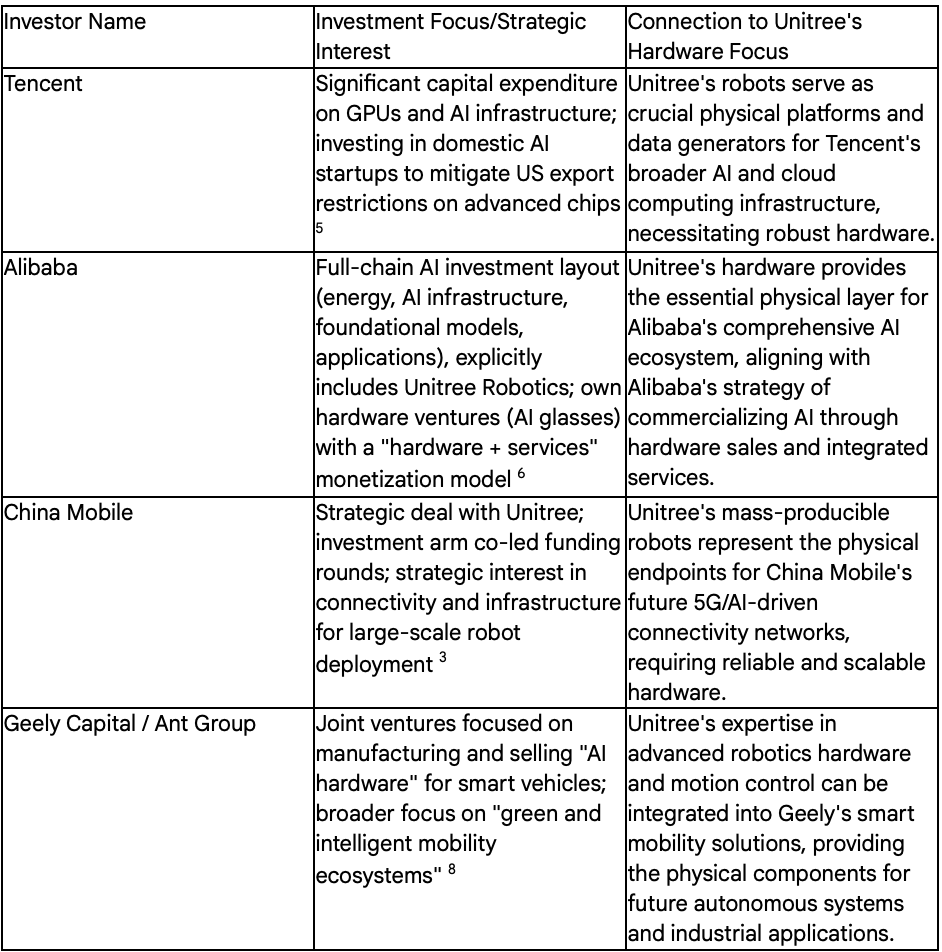

The Series C funding round was jointly led by a powerful consortium of major investors, including China Mobile's investment arm, Tencent, Alibaba, Ant Group, and Geely Capital. Notably, most of Unitree's existing backers also participated, indicating continued belief in the company's direction. Tencent's investment strategy includes substantial capital expenditure, with 76.8 billion yuan directed towards GPUs and AI infrastructure in 2024. Furthermore, Tencent is actively investing in domestic AI startups like DeepSeek to mitigate the impact of US export restrictions on advanced chips. Its investment in Unitree aligns perfectly with its broader objective of building out the physical infrastructure for AI, where robots serve as critical embodied AI platforms.

Alibaba's investment strategy features a "full-chain investment layout" that spans energy, AI infrastructure, foundational models, and applications, explicitly including Unitree Robotics within this comprehensive portfolio. Alibaba's own ventures into hardware, such as the Quark AI Glasses, demonstrate a clear belief in hardware sales as an initial commercialization pathway, followed by monetization through content subscriptions and value-added services, thereby forming a "closed-loop ecosystem of hardware + services". This strategic approach directly supports Unitree's hardware-first business model. Geely, in collaboration with Megvii, has established a joint venture specifically focused on manufacturing and selling "intelligent in-vehicle equipment" and developing "AI hardware" for smart vehicles. Geely's overarching digital transformation strategy centers on developing "green and intelligent mobility ecosystems". Their investment in Unitree positions them to integrate advanced robotics hardware into future smart mobility and industrial solutions. Unitree also secured a 46 million yuan deal with China Mobile , and China Mobile's investment arm co-led significant funding rounds. This indicates a strategic interest in the connectivity and underlying infrastructure essential for large-scale robot deployment, with Unitree's hardware providing the crucial physical endpoints for such networks.

Robotics funding is increasingly consolidating among fewer, more established players who receive larger investment checks. Investors are "increasingly concentrating their bets on established players rather than spreading across many startups". Companies that can demonstrate "proven hardware capabilities" are commanding premium valuations , indicating a clear market preference for tangible, scalable physical products. While "AI-native platforms" may achieve higher revenue multiples, the fundamental ability to deliver robust hardware is an indispensable prerequisite for attracting significant capital in the robotics sector.

Unitree's investor base, comprising major Chinese tech and industrial giants, represents a profound strategic commitment to building out the physical layer necessary for the widespread deployment and effective training of embodied AI.Alibaba's "full-chain investment layout" explicitly includes Unitree Robotics alongside investments in energy and AI infrastructure. Similarly, Tencent's substantial capital expenditure is heavily directed towards GPUs and core AI infrastructure. Furthermore, Geely and Ant Group are actively forming joint ventures to manufacture AI hardware specifically for smart vehicles. These investments transcend mere financial speculation; Unitree's robots serve as the crucial "edge devices" or "physical endpoints" for these investors' broader AI and smart ecosystem ambitions. By investing directly in Unitree's hardware capabilities, these corporate giants are securing a foundational piece of the future AI infrastructure, ensuring a reliable supply of affordable, scalable robots that can generate essential data and execute tasks in real-world environments. This strategic move directly mitigates the "hardware challenges" that are explicitly noted to "still hinder wider deployment" of AI models. Unitree is emerging as a critical enabler for the ambitious AI strategies of China's tech behemoths. This implies that Unitree's success as a hardware company is intrinsically linked to the broader national push for AI dominance. The investors are, in essence, betting on Unitree to become the leading provider of the physical "bodies" for the AI "brains" they are developing or integrating, thereby fostering a symbiotic relationship where hardware scale drives AI progress, and advanced AI capabilities, in turn, drive demand for more hardware.

The trend in robotics funding indicates a concentration on "established players" that possess "proven hardware capabilities," which, in turn, allows them to "command premium valuations". This investment pattern stands in stark contrast to the often-speculative hype surrounding pure AI software or unproven conceptual ventures (e.g., the case of Manus, which failed due to immature technology and high costs). While AI is undeniably critical for the future, investors are clearly prioritizing companies that can first deliver tangible, reliable physical products. The inherent complexity and significant capital intensity involved in robotics hardware development mean that investors are strategically de-risking their portfolios by backing companies that have already demonstrated a robust ability to produce functional, high-performance robots at scale. Unitree's extensive history of developing and successfully selling quadruped robots , coupled with its rapid and successful expansion into humanoids with competitive specifications , provides this crucial proof of capability. This strong focus on proven hardware significantly reduces the execution risk for investors. This prevailing trend in investment firmly solidifies Unitree's hardware-centric identity. It implies that in the robotics sector, the ability to consistently build and mass-produce robust, cost-effective physical robots is a more immediate and tangible measure of success and investment-worthiness than speculative AI breakthroughs. The market, in essence, values the "body" before the "brain" can fully develop and prove its commercial viability at a mass scale.

Table 2: Key Investor Alignment with Hardware/Manufacturing Focus

This table clearly and concisely lays out the strategic motivations of Unitree's key investors, demonstrating that their backing is not merely financial but is deeply and explicitly aligned with the hardware and manufacturing aspects of robotics. The table provides strong external validation for Unitree's hardware-centric strategy. When major tech and industrial players, with their vast resources, market insights, and strategic foresight, choose to invest significantly in a company's physical product capabilities, it signals a powerful endorsement of that strategic direction. The table effectively illustrates how Unitree's hardware can be integrated into the broader, interconnected ecosystems of these influential investors (e.g., becoming a foundational component within Alibaba's AI infrastructure or Geely's smart mobility solutions). This highlights the potential for Unitree's robots to become critical, foundational components in larger, interconnected systems, thereby driving sustained demand for its physical products. The involvement of such powerful corporate entities suggests a significant de-risking of Unitree's path to scale. Their implied access to advanced manufacturing capabilities, robust supply chains, and extensive distribution channels will be absolutely crucial for Unitree to achieve the high-volume production necessary for true hardware dominance in the robotics market.

4. Team Capabilities: Engineering Prowess and Hardware Innovation

Unitree Robotics was founded by Wang Xingxing in 2016. His foundational work dates back to his postgraduate studies (2013-2016), during which he developed 'XDog', a robot dog that "pioneered the technical solution for low-cost, high-performance autonomous robots globally". This early research and development focused on core engineering aspects, including control simulation, Permanent Magnet Synchronous Motor (PMSM) selection, Printed Circuit Board (PCB) design, and single-leg mechanical design. Wang's decision to leave his position at DJI to establish Unitree underscores a strong entrepreneurial drive rooted deeply in hardware innovation and a clear vision for the robotics industry.

Unitree "attaches great importance to research and development, and thus independently developed the motors, reducers, controllers, and even some sensors of the quadruped robot". This significant vertical integration of critical components is a defining characteristic of a hardware-centric company, enabling superior cost control, optimized performance, and rapid iteration cycles. The detailed product specifications for models like the G1 and H1 explicitly mention the use of "industrial grade crossed roller bearings," "low inertia high-speed internal rotor PMSM" motors, dual encoders, and advanced sensing components such as 3D LiDAR and depth cameras. This granular focus on mechanical and electronic components highlights a profound engineering-driven approach to their product development.

Wang Xingxing has explicitly stated that "hardware still needs to be cheaper, be larger-scale and more reliable" for achieving mass deployment. This strategic imperative directly aligns with the company's aggressive pricing strategy and its ambitious goal of making robots "accessible through leasing programs for factories, farms or households". Despite their robots often gaining attention for "showmanship" (e.g., performing dances at galas), Wang clarifies that the "team working on practical robotics is the largest within Unitree". This internal allocation of resources demonstrates a strong, underlying commitment to developing functional, deployable hardware solutions for real-world applications.

While Wang Xingxing acknowledges that "embodied AI remains inadequate" and awaits a "ChatGPT moment" for a breakthrough , he concurrently asserts that "Current robot hardware is sufficient". This nuanced perspective implies that Unitree has successfully established a robust hardware foundation, which now allows them to dedicate significant resources to AI development on top of this stable and capable physical platform. Unitree is actively developing its "UnifoLM (Unitree Robot Unified Large Model)" and exploring innovative "video-driven models" for robot control. The integration of NVIDIA Jetson Orin in the G1 EDU model further underscores their commitment to incorporating high-performance computing capabilities directly within their hardware platforms. The description of the Go2 robot dog as a "mobile platform to experiment with AI and control systems" clearly illustrates how Unitree's hardware products serve as essential testbeds and enablers for advancements in AI.

Unitree explicitly states that it "independently developed the motors, reducers, controllers, and even some sensors". This indicates a high degree of vertical integration for critical components. This level of in-house component development is a significant differentiator, as many robotics companies rely on third-party suppliers for these core, often expensive, parts. This internal capability was a key factor in the early success of Wang's XDog, which "pioneered the technical solution for low-cost, high-performance autonomous robots globally". By controlling the design, engineering, and often the production of these critical, high-cost components, Unitree gains substantial advantages in cost reduction, quality control, and performance optimization. This direct control over the bill of materials and the manufacturing processes is absolutely essential for achieving the aggressive price points (e.g., R1 at $5,900) necessary for market commoditization.Furthermore, it allows for more rapid iteration and customization of their hardware designs. This strategic choice firmly positions Unitree as a true hardware manufacturer, rather than simply an assembler of third-party components. It empowers them to directly address and drive down the "cost of hardware" , which is a major concern for industrial users, and to build a "larger-scale and more reliable" product base. This internal capability represents a core competitive advantage that fundamentally underpins Unitree's ability to become a dominant hardware provider in the global robotics market.

Unitree's CEO, Wang Xingxing, makes a critical distinction: "Current robot hardware is sufficient but embodied AI remains inadequate". He further emphasizes that "Hardware still needs to be cheaper, be larger-scale and more reliable" for mass deployment , even while identifying the "biggest obstacle to mass deployment is the embodied-intelligence AI model". At first glance, this might appear to be a contradiction: if AI is the primary bottleneck, why the continued emphasis on hardware? However, the underlying reality is that advanced AI models, particularly those designed for embodied intelligence, require vast quantities of real-world data and robust physical platforms for effective experimentation, training, and deployment. Unitree's strategy is to proactively provide the physical platforms (the hardware) that are indispensable for the anticipated "ChatGPT moment" in embodied AI to occur. By making these robots affordable and widely available—both as developer platforms and for industrial applications—Unitree is actively creating the necessary conditions for AI advancements. This approach ensures that when the AI breakthroughs do occur, Unitree will already possess the scalable hardware infrastructure ready for immediate, widespread deployment.

5. Policy Environment: Government Support for Hardware Manufacturing and Self-Reliance

The Chinese government's strategic initiatives play a pivotal role in fostering Unitree's growth as a hardware company. The "Made in China 2025" national strategic plan, launched in May 2015, aims to transform China from a producer of cheap, low-tech goods into a "world-leading manufacturing power". Robotics is explicitly identified as one of the 10 key sectors within this policy, with goals including increasing domestic content of core materials to 70% by 2025 and achieving self-reliance in high-tech products. This initiative has seen massive investments, estimated to be "hundreds of billions of dollars" in state funding, low-interest loans, and tax breaks, with an additional $1.4 trillion invested post-COVID-19.

Further reinforcing this commitment, the 14th Five-Year Plan and its related sub-strategies, alongside the "14th Five-Year Robotics Industry Plan" released in December 2021, prioritize robotics development, setting a goal to become a global robotics leader by 2025 with an annual industry growth rate exceeding 20%. Local governments in cities like Shenzhen and Beijing are amplifying this push, with Shenzhen aiming to cultivate a $14 billion robotics ecosystem by 2027 and Beijing targeting 10,000 humanoid robots in mass production by the same year. This supportive environment, including tax incentives and streamlined regulatory approvals, creates a fertile ground for companies like Unitree to accelerate commercialization and scale. Unitree's recent corporate restructuring from a limited liability to a joint-stock company aligns with these national goals, signaling readiness for public market scrutiny and large-scale operations.

China's national strategy provides a clear advantage in humanoid robotics development, as noted by Jeff Burnstein, president of the Association for Advancing Automation (A3). He highlights that China is "by far the biggest user of robots in the world," with a government committed to funding programs, a wealth of engineering talent, AI expertise, and manufacturing capabilities. This creates an ideal environment for Chinese companies to deploy robots domestically. The divergence in development paths between China and the US is also notable, with China moving much faster to deploy humanoids in factories, learn from real-world use, and iterate to more advanced models, compared to the US where pilot programs are more common. This strategic patience, building capabilities over 20+ years, positions China as a serious competitor in the high-stakes humanoid robotics market.

The Chinese government's "whole-of-nation" approach to AI and robotics, particularly the emphasis on "self-reliance and self-strengthening" and building an "independent and controllable" ecosystem across hardware and software, is a direct response to US export controls on advanced chips. This policy environment significantly de-risks Unitree's hardware-centric strategy by ensuring a protected domestic market and fostering the development of local supply chains for critical components. The substantial state funding and incentives for robotics manufacturing reduce the financial burden and accelerate the scaling of production for companies like Unitree. This also provides Unitree with a competitive advantage by allowing it to focus on cost-effective, high-volume hardware production without being overly reliant on foreign suppliers for core components, aligning with the "Made in China 2025" goals for domestic content. The government's push for mass deployment in factories and households further creates a guaranteed domestic market for Unitree's hardware. This policy-driven demand and support for indigenous manufacturing create a powerful flywheel effect, where government incentives drive hardware production, which in turn feeds into the national strategy for AI and industrial upgrading.

The government's active promotion of public engagement with robotics, such as the World Humanoid Robot Games in Beijing where Unitree's H1 robot took first place , serves a dual purpose. Firstly, it inspires children to pursue careers in robotics, ensuring a future talent pipeline for companies like Unitree. Secondly, it cultivates public acceptance and enthusiasm for robots, which is crucial for the eventual mass adoption of humanoid robots in everyday life, as envisioned by Unitree's CEO. This societal buy-in, fostered by government-backed events and public demonstrations, creates a favorable social and cultural environment for the widespread deployment of robotics hardware. This contrasts with regions where public skepticism or fear of automation might hinder adoption, providing Chinese companies with a unique advantage in scaling their physical products into diverse applications.

Conclusion

Unitree Robotics is definitively positioning itself to become a hardware company, driven by a confluence of strategic market decisions, robust internal capabilities, aligned investor interests, and a profoundly supportive national policy framework. The company's aggressive pricing strategy, exemplified by the R1's cost-effectiveness, is not merely a sales tactic but a deliberate move to commoditize robotics hardware, mirroring the successful market penetration playbook of DJI. This approach aims to establish a vast installed base of physical robots, which then serves as the foundation for future software and service monetization.

The backing from major Chinese tech and industrial giants, including Tencent, Alibaba, China Mobile, and Geely Capital, underscores a collective strategic bet on the physical infrastructure of AI. These investors view Unitree's robots as critical embodied AI platforms, essential for their broader ecosystem ambitions in cloud computing, smart mobility, and AI applications. This concentrated funding on companies with "proven hardware capabilities" validates Unitree's focus on manufacturing excellence and cost leadership in physical robotics.

Unitree's internal team, led by founder Wang Xingxing, possesses deep engineering prowess, evidenced by its in-house development of core robot components. This vertical integration provides unparalleled control over cost, quality, and performance, directly enabling the production of robust, low-cost, and reliable hardware necessary for mass deployment. The company's nuanced approach to AI, acknowledging current limitations while proactively building the indispensable hardware platforms, positions it to capitalize on future breakthroughs in embodied intelligence.

Finally, the pervasive support from the Chinese government, through initiatives like "Made in China 2025" and the 14th Five-Year Plan, provides an unrivaled enabling environment. This includes substantial funding, a focus on self-reliance in core components, and a strategic push for mass deployment of intelligent robots across industries. This top-down policy support significantly de-risks Unitree's hardware-centric strategy, fostering a domestic market and supply chain that accelerate its path to global dominance in robotics manufacturing.

In synthesis, Unitree's trajectory is a calculated move to own the physical layer of the burgeoning robotics market. By prioritizing the production and widespread distribution of affordable, high-performance robotic hardware, Unitree is not just building robots; it is building the foundational infrastructure upon which the future of embodied AI will operate, thereby solidifying its identity as a quintessential hardware company.