What Founders Can Learn from Unitree Robotics’ IPO Prospectus

Published:

Originally published on Substack.

Source: 002178_20260320_QY8F.pdf — Unitree Robotics Co., Ltd. IPO Prospectus (Application Draft)

Founder: Wang Xingxing (王兴兴) | Founded: August 26, 2016 | IPO Filing: March 2026

Yong’s Industry Memorandum | Updated May 2026

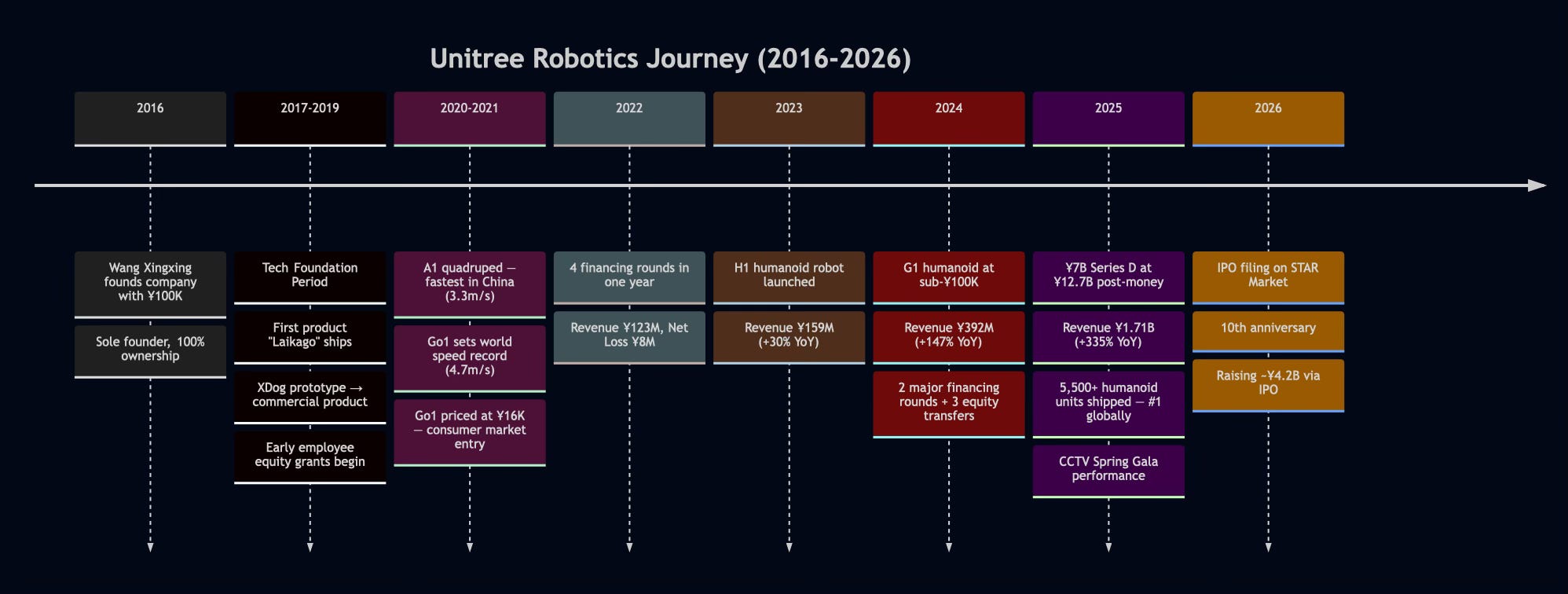

Unitree Robotics recently filed for its STAR Market IPO, disclosing hundreds of pages of application materials. This is not just a regulatory financial filing, but a highly practical playbook of hard-tech survival. Founder Wang Xingxing spent 10 years scaling a garage operation started with ¥100,000 to an expected IPO valuation of ¥42 billion (~$6.2 billion) and the world’s leading humanoid robot shipment volume. In August 2025, I wrote an article Unitree’s Trajectory Towards Dominance in Robotics, noting: Unitree is following in DJI’s footsteps, positioning itself as a hardware-led company that leverages China’s manufacturing advantages to capture the market. It has been proven that this positioning successfully enabled Unitree to become the first—and currently the world’s only—profitable humanoid robot company. Post-IPO, Unitree will venture deeper into industrial scenarios and utilize crowd-sourced data to build better AI model ecosystem products.

Zooming past the high-level AI hype, the most compelling part of the prospectus is its micro-level corporate architecture. The real story is written in these operational details. Unitree has built a world-class hardware, software, and developer ecosystem, with CEO Wang Xingxing concurrently serving as Chief Product Officer (CPO). A hard-tech startup must have a dedicated CPO—either the founder themselves, or someone with the actual budget and authority to drive product execution.

Unitree is a hard-tech benchmark that succeeded under extreme uncertainty. Behind its success lies the reality of hundreds of similar robotics startups that failed due to wrong technology roadmaps, cash flow collapses, or supply chain traps. Unitree’s breakout is not only due to its brilliant micro-level corporate design but also a favorable macroeconomic window. Nonetheless, its practices in equity defense, in-house cost reduction, dual-track product portfolios, and ESOP design remain a highly replicable hard-tech survival template.

10 Key Observations and Data Points from Unitree’s Journey

Commercializing prototypes over pitch-deck ideas

Evidence: Wang built the XDog prototype at Shanghai University and founded Unitree directly to commercialize it, bypassing the PPT concept phase.

Retaining manufacturing and design of core parts

Evidence: Self-developed integrated joints, torque motors, algorithms, and sensors rather than outsourcing them.

Remaining patient during the foundational period

Evidence: Spent four years (2016-2019) in pure R&D, keeping commercial revenues to a minimum to focus on component iteration.

Deploying a dual-track product strategy

Evidence: Go series quadrupeds lock in supply chain scale, while enterprise B/G/H series units secure high-margin enterprise sales.

Going global from Day 1

Evidence: Export revenue exceeded 55% of total sales for several years, de-risking domestic price wars.

Sequencing financing stages

Evidence: Credibility-focused early VCs (Sequoia, Matrix), followed by strategic buyers (Meituan), and pre-IPO backing from national giants (China Mobile, Tencent).

Accessing liquidity concurrently with primary financing

Evidence: Wang sold ¥50M in secondary shares at the primary round price during the Series D financing to relieve personal debt stress.

Deploying dual-class shares early to protect control

Evidence: Set up special voting rights when shareholding diluted to 23%, retaining 65% voting control post-IPO.

Filing for IPO only after proving self-sustainability

Evidence: Delivered ¥672 million in net operating cash flow and ¥600 million in non-recurring net income in 2025.

Funneling proceeds into future technology

Evidence: 74.5% of the target ¥4.2B IPO proceeds will go directly to AI model and next-gen hardware R&D.

I. The Story Arc: From ¥100K to ¥42B Expected IPO Valuation

II. Technical and Product Strategy: Beating the Market with Hardware Realism

1. Conviction Over Hype: The 4-Year Foundation

Wang Xingxing built his quadruped prototype (XDog) at Shanghai University using a pure hard-tech roadmap. He didn’t start with pitch decks to raise seed money; he immediately commercialized the hardware.

Technically, Unitree’s joint design inherits the “Quasi-Direct Drive” (QDD) philosophy pioneered by the MIT Biomimetic Robotics Lab—combining a high-torque-density motor with a low-reduction planetary gearbox to enable high-bandwidth torque control. Wang referenced open academic literature on these design principles during XDog’s early development (2013-2015). However, when MIT open-sourced its Mini Cheetah scheme in 2019, Wang noted that their motor and electronic configuration was highly similar to the design he had independently developed and published for XDog three years prior. Unitree’s core contribution was not inventing this QDD academic concept from scratch, but rather executing extreme cost reduction, engineering reliability, and mass manufacturing to transition it from a laboratory prototype into a commercial product.

In my observation of the hardware ecosystem, Unitree spent its first four years (2016-2020) in the workshop with almost no revenue growth. They developed their own motors, reducers, and control algorithms from scratch. While many hype-driven teams dismissed this approach as too slow, this early hardware experience determined the design parameters for their future humanoid systems.

Unitree’s Development Path vs. Conventional Robotics Teams

Entry Point:

Unitree: Developed the XDog prototype independently during grad school, transitioning directly to production upon graduation.

Others: Follow academic paper concepts → assemble pitch decks → seek VC funding to validate ideas.

First Product:

Unitree: Launched Laikago (2017) — a commercialized quadruped with a real BOM (bill of materials) and immediate shipping capacity.

Others: 3D renders, acrylic-housed laboratory demos, or conceptual MVPs.

R&D Depth:

Unitree: Full-stack R&D across core hardware (motors, gearboxes) and low-level control systems.

Others: Outsource hardware assembly, focusing only on high-level application software.

Foundational Patience:

Unitree: Weathered a 4-year (2016-2020) pure R&D phase with minimal commercial revenue.

Others: Seek to complete product cycles and scaling within a year of funding.

The joint modules of the H1 and G1 humanoid systems are fundamentally a combination of high-density frameless motors and precision reducers, which shares the same physical foundation as quadruped drive units. This development timeline cannot be bypassed. If they hadn’t spent years addressing CAN bus packet drops, gearbox tooth wear, and driver board overcurrent issues on quadruped platforms, the system complexity of launching a humanoid robot would have been unmanageable.

2. Full-Stack Self-Development as a Cost Control Lever

Unitree’s prospectus repeatedly highlights “全栈自研” (full-stack self-development) as its core moat. In deep tech, full-stack design isn’t about manufacturing every bolt; it is about strategically owning the components that determine the final BOM (bill of materials) cost and product performance, while keeping supply chain integration flexible:

Core Actuation & Joints: Unitree owns the core power module—integrated joint assemblies, frameless torque motors, and control driver boards. For planetary and harmonic reducers, while they maintain internal R&D and manufacturing capacity, they also integrate local suppliers (e.g., Zhongdali De and Green Harmonic) to share production volume.

Perception Modules: A hybrid strategy of “in-house design + off-the-shelf procurement” is utilized. For instance, Unitree developed its L1 4D LiDAR, but integrates industrial DJI (Livox) LiDARs on premium enterprise configurations to balance engineering speed and cost.

Control Loops & System Software: The motion control stack extends down to FOC magnetic field control, thermal dynamics simulation, and power management driver layers, avoiding black-box proprietary solutions.

Brain Models: Open-sourced UnifoLM (Unified Large Model) models (such as the WMA-0 world model for simulation, the VLA-0 vision-language model for natural language, and the WBT teleoperation dataset) cultivate the developer ecosystem, while the industrial UnifoLM-X1-0 model is tested directly on their joint assembly lines.

In the early phases, outsourcing speeds up time-to-market, but at scale, component markup eats all margins. Self-developing the critical motors and motion loops allows a startup to control pricing rather than leaving margin on the table for component suppliers.

3. The Dual-Track Product Matrix: Volume and Margins

Unitree avoided the trap of choosing between high-end research and low-cost manufacturing. Instead, they built a dual-track portfolio:

The Dual-Track Product Portfolio

Laikago (2017) | Academic Research

Pricing/Margin: Premium pricing / Academic exploration

Strategic Purpose: Proved quadruped dynamics and closed the control loop.

A1 (2020) | STEAM Education

Pricing/Margin: Mass-market entry

Strategic Purpose: Scaled up early batch assembly lines and tested consumer demand.

Go1 (2021) | Mass Consumer

Pricing/Margin: ¥16,000 (disrupted industry pricing)

Strategic Purpose: Drove down entry costs to quickly scale supply chain volume.

B1 (2022) | Industrial Inspection

Pricing/Margin: High premium / IP67 dustproof & waterproof

Strategic Purpose: Captured high-margin enterprise inspection clients.

Go2 (2023) | Consumer

Pricing/Margin: ¥9,997 (sub-¥10K retail)

Strategic Purpose: Minimal BOM cost; established global consumer volume monopoly.

B2 (2023) | Specialized Industry

Pricing/Margin: High premium / Explosion-proof and disaster response

Strategic Purpose: Replaced expensive foreign imports for power grid/utility clients.

H1 (2023) | Labs & AI Research

Pricing/Margin: Premium full-size humanoid

Strategic Purpose: Established early positioning and brand mindshare in the humanoid space.

G1 (2024) | Humanoid Research & Mass Market

Pricing/Margin: Sub-¥100K (¥99K starting price)

Strategic Purpose: Capitalized on supply chain advantages to capture global developer market share.

This dual strategy is highly effective: consumer-grade units (Go-series, G1) drive volume, establish ecosystem scale, and amortize fixed tooling/purchasing costs; enterprise-grade units (B-series, H-series) capture high ASPs and secure fat margins.

III. Financials and Product Economics: The Path to Profitability

1. Revenue Trajectory

2022: Revenue: ¥122.9M | Gross Margin: 44.18% | Net Profit: -¥22.1M | Adj. Net Profit: -¥8.1M

2023: Revenue: ¥159.1M (+30% YoY) | Gross Margin: 44.22% | Net Profit: -¥11.1M | Adj. Net Profit: -¥18.0M

2024: Revenue: ¥392.4M (+147% YoY) | Gross Margin: 56.41% | Net Profit: ¥94.5M | Adj. Net Profit: ¥77.5M

2025 (Q1-Q3): Revenue: ¥1,167.5M | Gross Margin: 59.45% | Net Profit: ¥105.3M | Adj. Net Profit: ¥430.6M

2025 (Full Year): Revenue: ¥1,708.2M (+335% YoY) | Gross Margin: 60.27% | Net Profit: ¥287.6M | Adj. Net Profit: ¥600.1M

(Note: The 2025 net profit was affected by a one-time share-based payment of ¥349M. The adjusted net income represents its true operational profitability.)

Unitree ran moderate losses in 2022 and 2023. They achieved profitability in 2024 (¥77.5M adjusted net profit) and reached ¥600M in adjusted net profit in 2025. They filed for IPO only after proving their cash-generation engine.

2. Component Scaling and Shifting Product Mix

Improving gross margins from 44% to over 60% in three years illustrates the economic levers of hardware scaling:

Amortization of self-developed parts: Internal component costs (motors, drives) drop rapidly as manufacturing volume increases.

Shift to high-ASP units: The high-margin humanoid business grew from nothing to 51.53% of revenue (¥595M) in Q1-Q3 2025, while quadrupeds dropped to 42.25%.

The financial logic here centers on using the cash flows and supply chain scale of a mature product (quadrupeds) to fund the development of the next-generation platform (humanoids). Because the two lines share core motor and control systems, reusing these technologies lowers technical risk and expands net margins.

3. Global Revenue as a De-Risking and Margin Engine

2022: Overseas Revenue: ¥69.4M | 57.2% of total revenue

2023: Overseas Revenue: ¥87.6M | 55.6% of total revenue

2024: Overseas Revenue: ¥215.7M | 55.7% of total revenue

2025 (Q1-Q3): Overseas Revenue: ¥452.8M | 39.2% of total revenue

Relying on a single domestic market limits a startup’s options. Unitree maintained overseas revenue above 55% for years. Even with the domestic humanoid spike in 2025, international sales grew to ¥452.8M. Overseas research and enterprise buyers are far less price-sensitive, providing higher ASPs and buffer margins that fund the domestic cost-reduction roadmap.

IV. Capital Efficiency: Sequencing High-Quality Funding

1. Financing Round History

Pre-2022 (Seed/Angel & Pre-A):

Investors: Sequoia China, Astrend IV (Source Code), Matrix Partners, Vertex Ventures, Decent Capital

Capital Raised: Undisclosed

Valuation: Estimated at ~¥200M to ¥500M post-money

January 2022 (Series A):

Investors: Matrix Partners, Hexagon, ESOP platform

Capital Raised: ¥91.5M

Valuation: Implied post-money of ~¥900M

March 2022 (Series A+):

Investors: Local state funds, Astrend IV (Source Code) follow-on

Capital Raised: ¥108.4M

Valuation: Implied post-money of ~¥1.1B

June 2022 (Capitalization):

Action: Conversion of capital reserve to share capital (8x increase in shares)

Valuation: Bookkeeping restructure for subsequent joint-stock conversion

June 2024 (Series B):

Investors: Meituan (Hanhai), CITIC Goldstone, Source Code Capital, Xinjiang Shenzhen Capital

Capital Raised: Undisclosed

Valuation: Valued at ~¥7B to ¥8B post-money

August 2024 (Series C):

Investors: Beijing Robot Fund, Zhongguancun Science Park, Sequoia Capital, CITIC Securities

Capital Raised: ¥284.7M

Valuation: Valued at ~¥8B to ¥10B post-money

June 2025 (Series D):

Investors: China Mobile (Zhongyi Hechuang), Tencent, Wuxi Jinqiu, and 23 existing investors

Capital Raised: ¥694.5M (plus secondary shares)

Valuation: ¥12.0B pre-money / ¥12.7B post-money

2026 (STAR Market IPO - Planned):

Investors: Public offering and strategic placement

Target Raising: ~¥4.2B

Valuation: Expected IPO listing valuation of

¥42B ($6.2B)

2. Sequencing the Investor Base

Looking closely at Unitree’s cap table shows a logical sequencing of capital partners:

Early Stage (2016-2021) — Credibility: Top-tier financial VCs (Sequoia, Matrix, Vertex) established the brand’s reputation, opening doors to university and research institute procurement.

Growth Stage (2022-2024) — Order Volume: Commercial and industrial strategic partners (like Meituan) entered to validate real-world scenarios such as deliveries and logistics.

Late Stage (2024-2025) — Ecosystem Scale: Big tech and state-backed funds (China Mobile, Tencent, municipal robot funds) laid the groundwork for large-scale industrial deployment and major integration project bids.

Every round was structured to prepare for the next stage of commercial rollout.

3. Clean and Concurrent Founder Liquidity

During the June 2025 Series D round, Wang Xingxing sold 11,378 shares to Source Code Capital for ¥50M.

In the Series D round with a valuation exceeding ¥10B, a ¥50M secondary sale is standard practice. Ten years of hardware development is a long grind, and a founder’s personal finances are under high stress. Relieving this pressure with a transparent secondary transaction allows the team to maintain strategic focus, preventing short-term decisions after listing. However, such liquidity events require the founder to maintain absolute voting control. This is a crucial lesson for all founders: without early defenses, dilution will leave you vulnerable during growth rounds, potentially resulting in a loss of corporate control and hindering future development.

V. STAR Market Listing and Corporate Architecture

1. Safeguarding Control via Dual-Class Voting

Unitree opted for the SSE STAR Market, utilizing a dual-class share structure:

Listing Criteria: Minimum expected market cap of ¥10B (met via ¥12.7B Series D valuation, with expected IPO valuation at ~¥42B).

Voting Power: Wang Xingxing holds direct A-class shares carrying higher votes (approx. 2.67 votes per share).

Control Line: Wang controls 68.78% of the voting power pre-IPO with 23.82% economic equity. Post-IPO, his voting power remains above 65.3%.

This voting control shields the engineering roadmap from being derailed by short-term market pressures, even when economic ownership drops below 25%.

2. Launching the IPO at the Intersection of Metrics and Brand

Unitree timed its filing when several key lines crossed:

Financial Strength: ¥600M in adjusted net profit in 2025, demonstrating solid self-funding capability.

Narrative Peak: Embodied AI and humanoid commercialization entered the late-stage testing phase globally.

Volume Leadership: Shipping 5,500+ humanoid units in 2025, establishing an undeniable volume lead.

3. Allocating IPO Proceeds to R&D

Unitree’s target ¥4.2B IPO proceeds are allocated as follows:

Intelligent Robot Model R&D: ¥2.02B (48.1%) — Embodied AI models, reinforcement learning, and cloud systems.

Robot Body R&D: ¥1.11B (26.4%) — Next-generation hardware dynamics.

New Product Development: ¥0.45B (10.6%) — Expanding the catalog.

Manufacturing Site: ¥0.62B (14.9%) — Expanding output.

Directing 74.5% of IPO proceeds to R&D signals to the public market that Unitree is an AI and robotics engineering platform, rather than an assembly-only business.

VI. Equity and ESOP Abstractions

1. Mitigating Dilution with Structured Voting Rights

Wang Xingxing’s ownership journey:

Founding (2016): Economic Ownership: 100% | Voting Power: 100%

Pre-2022 (Early VCs): Economic Ownership: ~41% | Voting Power: ~41%

Post-2022 Rounds: Economic Ownership: ~36% | Voting Power: ~36%

Post-2024 Rounds: Economic Ownership: ~27% | Voting Power: ~27%

Post-2025 Series D: Economic Ownership: 23.82% | Voting Power: 68.78% (established dual-class voting)

Post-IPO (Planned): Economic Ownership: 21.44% | Voting Power: 65.31%

In control defence, waiting until ownership drops below 30% to set up mechanisms is usually too late. Unitree incorporated AB dual-class voting in May 2025 during its transition to a joint-stock company. Resolving this structure early in the listing process avoids regulatory hurdles closer to IPO.

2. Avoiding Equity Proxy Pitfalls: The LP ESOP Structure

The prospectus details the cleanup of historical “equity proxy/nomination” arrangements.

Between 2017 and 2021, Wang held shares on behalf of 11 employees for privacy reasons. In listing audits, such proxy holdings are major red flags due to potential ownership disputes. In 2025, Unitree consolidated employee shares into the Shanghai Yuyi partnership platform.

From a governance perspective, proxy arrangements introduce severe compliance risks. A cleaner approach is using a limited partnership (LP) platform where the founder acts as the GP (general partner) and employees act as LPs (limited partners). The GP retains all voting power, while employees receive the economic returns. This rewards talent without fragmenting company control.

VII. Headcount and Organization

At the time of filing, Unitree had only 480 employees, generating approximately ¥3.56M ($490K USD) per employee. This is an exceptionally high efficiency rate for hardware manufacturing:

Revenue per employee: Approx. ¥3.56 million, putting the company at the top tier of structural hardware manufacturing.

R&D Makeup: The R&D team consists of only 124 people (37.8% of headcount). This lean engineering core developed and maintained multiple quadruped and humanoid lines.

Leadership Stability: The core technical leadership team (Yang Zhiyu, Chen Li, Zhang Yangguang) has been stable for 7 to 9 years, holding substantial stakes in the early ESOP.

In my experience, a flat and highly technical R&D structure avoids administrative overhead. Keeping the team flat and highly technical minimizes alignment friction and lets the founder stay close to the physical details.

VIII. Key Risk Exposures We Must Face

Unitree’s risk disclosures detail their real points of vulnerability, which are standard for the robotics sector:

Key Brain Dependency: Heavy reliance on Wang Xingxing and a small group of core technical experts.

Inventory Obsolescence: Holding ¥278M in inventory by Q3 2025. In a fast-moving engineering sector, component obsolescence can rapidly write down margins.

FX Exposure: With over 35% of revenue from international markets, currency fluctuations introduce cash flow volatility.

About the Author

涌 Yong — 20-year industrial automation and robotics veteran, former product lead at Spirit AI (valuation ¥20B+), three-time founder and exit in both the US and China (IIoT / AIGC / OSS). Currently focused on cross-border venture research in embodied intelligence and deep tech.

Personal Website: qianyong.me

Substack: yongqianme.substack.com

LinkedIn: linkedin.com/in/yongqian

X/Twitter: @yongqianme